How Much Profit Do Banks Make From Treasury Services

Getting Maximum Value From Your Bank Transaction Services Spend

Treasury Strategies, a division of Novantas, Inc. estimates that companies spend nigh $twenty billion per yr of bank treasury management services in the U.S. and more than $200 billion worldwide. Corporate treasurers who optimize their utilize of these services enjoy accelerated cash menstruum, improved adventure direction, college investment income and quality information, all at a reasonable cost.

Unfortunately, many treasury systems have evolved or take been put in place in a haphazard style. Some warning signs of inefficient use of bank transaction services include:

- In moving services from ane bank to another, companies fail to complete the migration.

- When companies merge, many do not take the opportunity to streamline their operating depository financial institution structures.

- Companies with decentralized or global treasury operations purchase redundant services or duplicate information from their banks.

- When companies upgrade to more advanced cash management services, they fail to turn-off the legacy service.

- Many companies use late-life cycle bank products that are no longer efficient.

- In their zeal to minimize banking company service fees, they do non accept advantage of value-added services and just stick with the plain vanilla.

- Companies who demand exception processing from their banks are probably paying dearly for the service while missing the benefits of newer, state-of-the-fine art treasury products.

- Companies that spread their services beyond many banks are probably operating sub-calibration.

- Companies with inefficient banking concern account structures are likely undisciplined at many levels.

In all these cases, companies are losing value. Some companies may exist overpaying for transaction banking services while others are missing scale opportunities and book discounts. Some may crave extra staff simply to do the reconciliations required by an inefficient depository financial institution account structure while others purchase redundant information services from their banks "merely to brand certain." Many leave excess balances on deposit at low earnings credit rates as a absorber for the errors that are sure to issue from a poorly designed treasury direction system. Worst of all, these poor practices expose companies to financial risks or fraud.

At Treasury Strategies, we work with our clients to help them systematically understand their banking needs and methodically establish a depository financial institution business relationship and services structure that uses best in course transaction banking services inside the constraints of the visitor's credit network, geography, organizational structure and, in some cases, their

regulatory framework.

The first stride in a banking services optimization is to catalog each of the major payment categories by part. In doing this, you will become a good handle on specific service requirements. That will help in identifying best in class transaction banks for your consideration.

- Inbound Commercial Payments settle sales of appurtenances and services between y'all and your concern customers. (B2B)

- Inbound Retail Payments settle sales of goods and services between you lot and your retail customers. (C2B)

- Outbound Commercial Payments settle purchases between you lot and your vendors.

- Intracompany Transactions motion funds between visitor accounts for either cash concentration or funding needs.

- Supply Chain Networks are regular and highly structured transactions with a smaller set of trusted vendors requiring all-encompassing data interchange, dynamic discounting or other types of highly integrated payments.

- Liquidity Management Transactions settle short term investment and borrowing needs.

- Capital Transactions are large and irregular payments for major balance sheet items such as capital appurtenances, real estate, capital markets activities and M&A.

Each functional dimension entails a different set service features that need to be paired with your banks' specialties. This list should brand clear that for almost companies, this is not i size fits all.

- The treasury information services required for intracompany greenbacks mobilization transactions are very dissimilar than those required for entering commercial payments. The former but requires info that the transfer has been completed while the latter requires extensive item for receivables cash application.

- Certitude of settlement criteria for upper-case letter transactions are much higher than for repetitive vendor payments.

- Gamble direction and fraud prevention services are more critical for college value, lower frequency outbound activities.

Later thoroughly documenting your requirements, you can brainstorm to identify the banks best suited for each action. This is usually done inside the constraints of your credit cyberbanking structure, geography or other organizational imperatives. Some companies prefer to conduct all-encompassing requests for proposals and bank fee negotiations. Others are quite successful with breezy bank presentations and discussions. Both methods tin piece of work. The primal, in addition to beingness systematic and methodical, is being equipped with good information. That means utilizing NDepth depository financial institution fee direction benchmarks in either approach.

Finally, once your bank account structure is optimized and your treasury management services are properly implemented at your transaction banks, there are several steps to take to ensure you proceed to get the nearly bang for the cadet. These components of a best in class bank fee management program support that goal:

- Brand sure you receive monthly account analysis statements from each of your transaction banks in an electronic format. We recommend either true PDFs, EDI 822s or TWIST BSB files. New technology is available to help corporate treasury managers read PDFs and avoid the more IT intensive EDI or TWIST files.

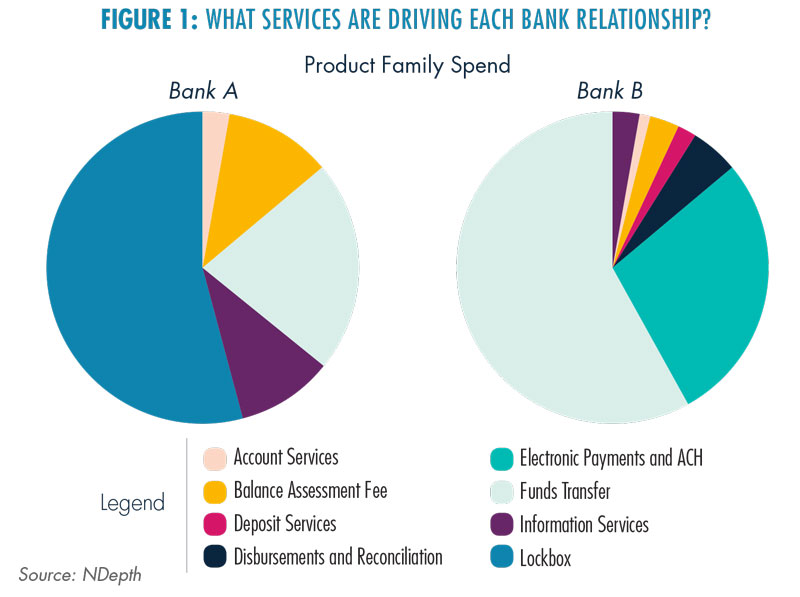

- Manage your bank services at a product family level. Banks use well over one m service codes in their product structure and their account analysis service billing. Not simply is it incommunicable to manage at that level of detail, it makes no sense. Many of those codes are just features or components of the complete product which cannot be unbundled. All those components demand to be managed as a package, a product family unit.

- Benchmark your depository financial institution fee pricing and earnings credit rates. You want to make sure you lot're paying a fair price for services that are critical to your business organisation. Some criterion services only ascribe an "average price" for each service line item. That completely misses the signal. Benchmarking needs to occur at the product family level and to incorporate volume scale. A fair toll for a low volume of a service is higher than for a higher volume of the same service.Only consider the chart that illustrates the scale dynamics of lockbox services (Figure 2). The $5.00/item this company pays for a low volume lockbox at Banking concern A is below the market place criterion. However, the $4.00/item it pays for a higher volume lockbox at Bank B is higher up the benchmark median. Without proper benchmarks (or with cocky-benchmarking), a treasury manager would reach a differ and incorrect determination.

- Use tools to monitor your monthly banking concern account assay statements. Many depository financial institution services billing statements run dozens of pages with hundreds of line items. Several banks brandish AFP Service Codes in an try to standardize, yet they are often inconsistently practical.

The sheer book of information defies rekeying into spreadsheets. Fortunately, advanced tools like NDepth can easily read your AA statements, validate and ingest your data, map into product families and benchmark against the market. - Go on a watchful eye on your data service charges. Information services is perhaps the trickiest product family to manage. Banking company and AFP service codes practice not fully capture the wide array of information services. Some are priced by module, others take monthly maintenance charges or daily transmission charges. Some are based on file size, others keystrokes. Further complicating matters is the proliferation of data commitment channels such as web portals, EDI, file transmissions, phone updates, email and text commitment, mail and courier. The best do is to understand these services, ensure yous pay for each piece of information but one time, and use the channel nearly effective for your business.

- Be mindful of services with high stock-still costs. Monthly maintenance fees, subscriptions, daily charges and fixed module charges are assessed whether y'all have one transaction in the production family or tens of thousands. We advise our clients to regularly examine these types of services and consolidate book whenever it makes business sense. Detect the median (red) line in the lockbox chart (Figure 2). This is a great illustration of how book scales. In fact, using extensive NDepth data, we take been able to calculate that lockbox product family unit pricing declines by 24% for every doubling of volume. That'south compelling. All transaction banking services exhibit these scale pricing dynamics at a product family level, at varying rates.

- Avert penalty fees. Banks charge for bad behavior then make sure you're buttoned upwards. Avoid overdrafts. Brand sure your funds transfer formats and your ACH files comply with Fedwire, SWIFT and ACH standards. Evaluate advisedly before asking for exception processing. Use electronic rather than paper-based services.

- Proceed in bear upon with your bankers to make sure you are adopting the bank's best, value-added services. There is no substitute for transparent, ii-manner advice in the transaction banking relationship. Nigh bankers are certified treasury professionals (CTPs or CCMs) past the Clan for Financial Professionals. Don't proceed them at arms' length. Allow them help you. Every bit we tell our clients, "It'due south your job to help your banks put their best foot forward."

Related Articles

Bank Fee Analysis, Ripe with Opportunity — New automated depository financial institution fee management solutions are providing state of the fine art tools and benchmarks. They even read PDF depository financial institution account analysis statements and avoid messy EDI 822 files. To relieve time and money, you tin at present just drag and drop.

Understanding Your Bank Fee Analyses — Bank Account Assay statements are daunting. U.S. companies spend $xx billion per year on transaction banking services, yet the bank services billing statements are indecipherable.

Corporate Treasury Priorities — Each year, Treasury Strategies assesses the state of the treasury profession and key bug on the horizon. Pinnacle priority for this yr is greenbacks forecasting, treasury systems and optimizing treasury technology. Top benchmarking need is bank service fees.

Earnings Credit Rates Rise at Uneven Stride — Getting an allowance on your residual depository financial institution balances can be a overnice source of income. Our NDepth earnings credit charge per unit benchmarks show wide variances for the 3rd quarter.

Making the Almost of Your Banking company Balances — Many corporate liquidity management programs overlook bank balances. This article explains the importance of ECR, compensating balances, bank sweep accounts and money marketplace funds.

If y'all'd like to receive more than data or a complimentary custom report, please contact ndepth_info@treasurystrategies.com

How Much Profit Do Banks Make From Treasury Services,

Source: https://treasurystrategies.com/industry_insight/getting-maximum-value-from-your-bank-transaction-services-spend/

Posted by: cashsyle1983.blogspot.com

0 Response to "How Much Profit Do Banks Make From Treasury Services"

Post a Comment